The Outlook for LNG as a Marine Fuel

Today, LNG-fuelled vessels amount to approximately 13% of the current newbuild order book and estimates for 2021 and beyond show continuing growth in many classes of vessels. Importantly, 2020 also saw the first uses of bio-LNG by deep-sea ocean vessels, thereby reducing the carbon footprints of these vessels.

The reasons for this expansion are clear. Ports and cities around the world are beginning to take the threat of air pollution and shipping’s contribution to it seriously. Air quality and human health awareness during this pandemic gained renewed interest and continues to be a key determinant of sustainable port activity. This coupled with the need to reduce the carbon footprint of the global maritime industry clearly points to the use of LNG to satisfy these aggressive but necessary goals.

Across the globe, 2020 has seen a profound shift in public opinion towards building back better and greener. Shipping companies that choose not to take positive action to meet essential environmental targets put their corporate reputations at risk, and will increasingly see negative impacts on financing, employee retention, customer satisfaction, and operational freedom.

Two options, one choice

While the air quality benefits of LNG have been known for years, a clear choice has now emerged for shipowners in how they will tackle decarbonization – the key strategic challenge that will define the decade ahead.

There are now less than ten years to achieve the initial 40% GHG reduction targets set by the International Maritime Organization (IMO) for 2030. 2020 was the year that the industry realised that fundamentally, there are really only two viable options for newbuild vessels as a means of reaching these IMO targets.

One is to use LNG, thereby gaining an immediate carbon reduction of up to 21% on a well-to-wake basis compared with current oil-based marine fuels over the entire lifecycle. In combination with design and operational efficiency measures, the initial 2030 target for GHG reductions can be met using LNG. Gradual introduction of bio-LNG and at a later stage, synthetic LNG, will incrementally decarbonise shipping towards IMO’s 2050 targets.

The only other alternative is to avoid making a decision and waiting for technologies to develop in the future. Waiting is a high-risk option; waiting means that shipping will continue to contribute more GHG than it would if it were using LNG today. The proposed alternative fuels we are waiting for are also far from proven. It is clear that global availability of these untested and developing alternative fuels is more than a decade away and are not therefore viable for 2030 compliance.

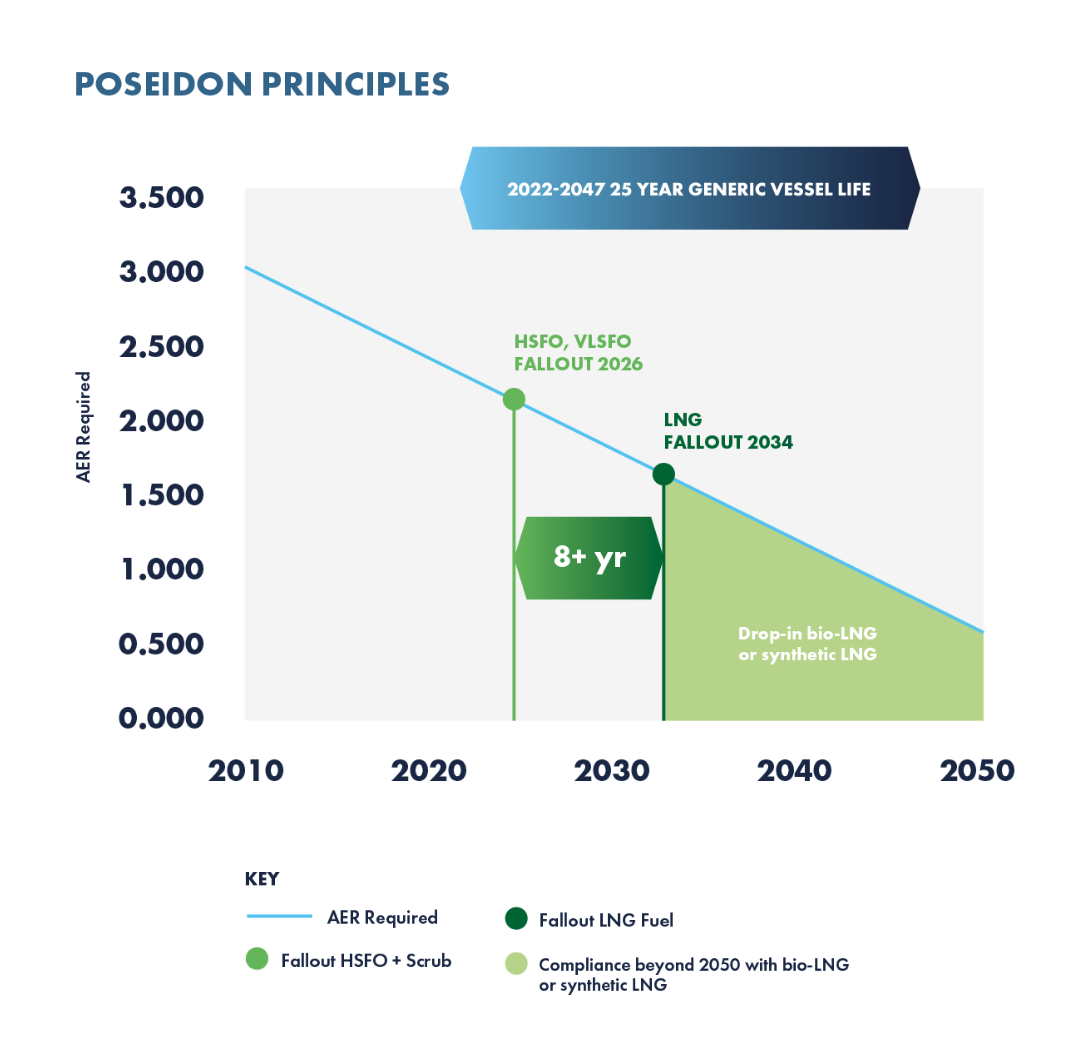

As banks increasingly align with green finance principles, LNG offers potential financing benefits. For example, it provides an ‘extended compliance runway’ under the Poseidon Principles, an initiative developed by key ship finance banks which attempts to align their investment portfolios with the IMO’s decarbonization targets. An investor can gain up to eight years of more favourable financing terms compared with vessel fuelled by conventional marine fuels such as HSFO, VLSFO, and MGO. The use of bio-LNG as a drop-in fuel can extend this even further. That means it is possible to start reducing emissions now and enjoy the benefits of Poseidon Principles-compliant finance for the longer term.

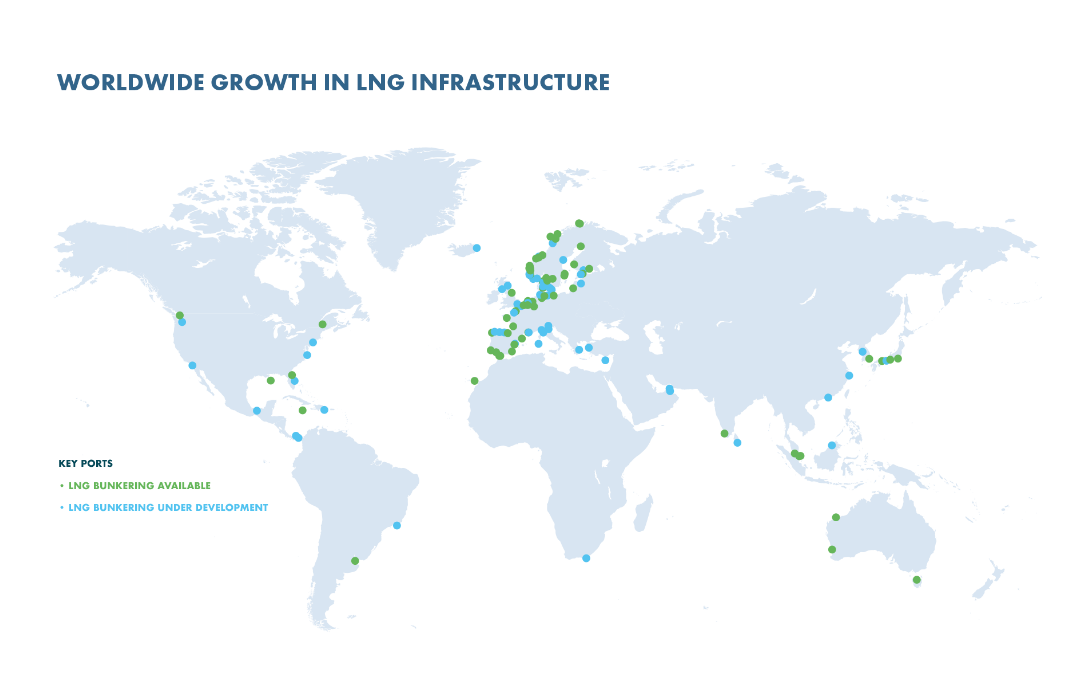

LNG infrastructure is growing almost daily and has a proven safety record over decades of use. LNG cannot pollute our seas and waterways, it is non-toxic, and ports around the world are facilitating the bunkering of this important fuel.

Bio-LNG and synthetic LNG

There are several options on the table when it comes to zero carbon fuels. Some may prove to be viable in the decades ahead offering the shipping industry a “basket of fuel options” to meet the targets. This basket is likely to include LNG and its bio and synthetic siblings.

Bio-LNG has emerged as a prime pathway to carbon neutrality. Unlike many other biofuels, bio-LNG derives from mainly waste and agricultural and forestry residues. It does not compete with food and other important agricultural products or contribute to deforestation. It is also chemically identical to fossil LNG and can therefore use the same engines, storage systems and bunkering infrastructure. Although availability is relatively limited today, there is massive potential as recognised by independent research organizations such as the IEA and CE Delft, and production is scaling rapidly on a global basis.

The production of bio-LNG can help solve another global environmental problem, what to do with our human-generated and animal waste products. This is another policy matter that cannot be underestimated or dismissed.

Longer term, synthetic LNG, produced through the well-established power-to-gas process, using the same renewable energy building blocks as green ammonia and other e-fuels, is likely to become available in increasing volumes as global renewable electricity capacity grows.

The use of LNG now paves the way for bio-LNG and synthetic LNG in the future, offering a future-proof investment for ship owners. LNG has a strong head start; it is available now with a fast-growing bunkering infrastructure; it has a proven safety record and its emissions benefits have been fully assessed on a full lifecycle (well- to-wake) basis.

Lifecycle analysis

Decision makers in the industry must ensure that they are comparing like with like when it comes to other options. They should not avoid the difficult questions. Will the seafaring and port communities accept the significant safety risks posed by some of these alternative fuels at scale? Will ports around the world be willing and able to adapt to bunkering of toxic or highly flammable substances? Who will pay for these reportedly trillion-dollar-plus supply and infrastructure investments? Are there less costly alternatives to achieve the same critical environmental goals?

Maritime customers are actively seeking cleaner and more environmentally appropriate means of transport. Globally, regulators, charterers, financiers, and beneficial cargo owners are actively demanding more sustainable and environmentally conscious shipping. As the pursuit for zero carbon has evolved, it is becoming clear that a “basket of marine fuels” will materialize. Shipowners must be given the right information and accurate data to enable them to make the right decisions for their fleet.

No fuel is perfect and there are always obstacles to overcome. Methane slip onboard some LNG-fuelled vessels and fugitive emissions in the LNG supply chain does occur. However, there are engine solutions operating today that have virtually no slip. Methane slip is a problem with a technical fix, rather than a fundamental issue with the fuel and technology. Further, new engine technologies that dramatically reduce levels of slip in other LNG engines are emerging quickly. Upstream developments are also advancing at pace with new regulations and industry initiatives. For example, the Climate & Clean Air Coalition (CCAC) Global Methane Alliance (GMA) was launched in 2019; 2020 saw the release of the new EU Methane Strategy; and the oil majors in the Oil and Gas Climate Initiative (OGCI), have committed to strong methane emissions reduction targets.

Decisions on future fuels must be made on a full lifecycle basis, specifically on a well-to-wake basis. Alternative fuels such as ammonia and hydrogen may emit no GHG when used in propulsion systems such as internal combustion engines or fuel cells but their overall, well-to-wake emissions depend on how they are produced. Only if they are produced from renewable energy such as wind and solar can they truly be ‘zero-emissions’ fuels. However, if they are produced from fossil fuels, as is the case now and for the foreseeable future, then their well-to- wake emissions can be far higher than those from fuels such as LNG.

Furthermore, fuels such as ammonia and hydrogen have major challenges to overcome before they can be safely used. For example, ammonia slip is a potential issue that must be addressed given the toxicity of the product. Similarly, there are very practical technical problems to overcome with super-cryogenic storage onboard of hydrogen, permeability and flammability. These matters are often overlooked in the current discussions but need to be addressed with urgency and seriously considered.

Without detailed lifecycle analysis, the unintended consequences of policy decisions and technology investments could develop into major concerns. Complete lifecycle analysis with current data taking actual operational environments into account and working with seafarers, ports and port communities is essential.

The future for maritime

The choice is clear. 2021 needs to be the year when owners and fuel suppliers who are serious about human health and decarbonizing shipping must act. Bio-LNG is a credible zero-carbon pathway with massive, unrealized potential.

Longer term, synthetic LNG, produced from the same renewable energy feedstocks as green ammonia and hydrogen, offers another zero-carbon option. We need global policymakers to recognise the potential of LNG and these other products and provide corresponding incentives to industry by:

- Adopting a goal-based, technology-neutral approach which guarantees a true level playing field between different fuel solutions on a lifecycle (well-to-wake) basis

- Integrating the bio dimension of LNG in any revisions to GHG emissions reduction targets for shipping to facilitate quick results

- Incentivizing and enhancing investment in bio-LNG production for the hardest-to-abate sectors such as shipping; and

- Creating a single market for biomethane and bio-LNG by facilitating trading of volumes and certificates across borders free of technical or political barriers.

For vessel owners looking to invest in new tonnage today, the choice is clear. You can start to reduce emissions now while protecting the future. Waiting for a zero-carbon alternative might seem attractive but the future is still a long way off and the technology required is not proven. Waiting for these to come to fruition would both exacerbate the growing GHG emissions issues and does not provide the essential air quality benefits derived from LNG. The journey of a thousand miles starts with a single step, and the sooner we start the journey the better.

that matters most

Get the latest maritime news delivered to your inbox daily.

Waiting is not an option.

Peter Keller is the chairman of SEA-LNG and the former executive vice president of TOTE, Inc. He has served on the boards of the Pacific Maritime Association (PMA), the Pacific Maritime Shipping Association and the United States Maritime Exchange (USMX), and he was inducted into the International Maritime Hall of Fame in 2006.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.