BIMCO: Chinese Shipyards Achieve Market Share Record in 2022

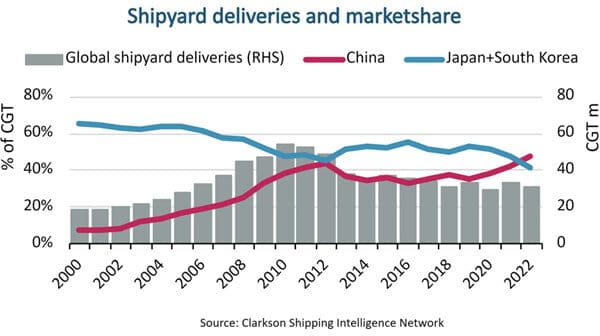

After decades after China began its concerted efforts to build its competitiveness in the global shipping industry, its shipyards hit a record 47 percent market share in 2022 according to a new analysis from the shipping trade organization BIMCO. According to their report, last year was the first time that Chinese shipbuilders exceeded the combined market share of Japanese and South Korean shipyards.

China initially attracted orders by offering lower costs focusing on the most basic of ships such as bulk carriers. They contributed to the shift away from Europe’s traditional shipbuilders to the lower costs found in Japan, South Korea, and ultimately China. More recently they have invested in new systems and processes to enhance productivity and now are beginning to make entries into the high-value, more complex segments including their first substantive orders for LNG gas carriers and using their first domestic cruise ship construction to develop expertise in the segment. China looks to leverage these competencies to compete in these segments still dominated by the South Koreans and European shipyards.

“Chinese shipyards’ success has been achieved by maintaining a leading position within dry bulk ships and, more recently, establishing themselves as the premier location for building container ships,” highlights Niels Rasmussen, Chief Shipping Analyst at BIMCO. While South Korea is leading with the orders for methanol dual-fueled containerships, China has come on quickly moving in 20 years from 5,000 TEU ships to this week when they are completing construction on two of the world’s largest containerships, each with a carry capacity of over 24,000 TEU. Just today, OOCL named its first new Chinese-built ultra-large vessel while several similar vessels are being readied for delivery to MSC from several Chinese shipyards.

According to BIMCO’s analysis of the data from Clarkson Shipping Intelligence Network, ships delivered to new owners by Chinese shipyards in 2022 totaled 14.6 million Compensated Gross Tonne (CGT), or nearly half of the 30.8 million CGT delivered globally. It is especially significant as China struggled with efforts to control the spread of COVID-19, which included lockdowns that impacted the shipbuilding cluster near Shanghai mostly in May 2022. Despite these disruptions to production, China delivered nearly twice as many CGTs as South Korea (7.8 million CGT). Japanese shipyards continued to slide with Clarkson reporting deliveries of just 4.8 million CGT. Combined South Korea and Japan delivered 12.6 million CGT.

China's market share has been growing consistently over the past 20 years. In 2000, Clarkson calculates they held less than 10 percent of the market, but in 2009 emerged as the market leaders. The last time that China approached the combined level of its next two rivals was in 2013 during the downturn in the shipbuilding industry.

Overall, the Chinese industry holds 45 percent of the global orderbook or 109.1 million CGT. By comparison, South Korea currently has 34 percent of the orders focusing increasingly on the high-value segments including dual-fuel and gas carriers. Japan has a 10 percent market share.

“They also hold a large share of orders for most other ship types but have yet to establish themselves as key players within the gas carrier sector,” notes Rasmussen. BIMCO however expects that it is possible that China could make inroads also into this sector, just like they gradually attracted orders for ultra large container ships.

that matters most

Get the latest maritime news delivered to your inbox daily.

LNG carriers are currently the second largest ship sector within the global orderbook for ships, and South Korean shipyards remain the market leaders within this sector, holding 79 percent of the order book. Currently, Chinese shipyards hold only 15 percent of the LNG carrier orderbook.

Despite China’s success, BIMCO however warns that cost increases could threaten China’s longer-term position. They point to the potential that lower cost countries like Vietnam and the Philippines could become larger competitors in the future similar to how the center of shipbuilding historically moved from Europe to Japan and onwards to South Korea and China.