The Ship Mortgage Crisis

How ship valuation methods rationalized toxic shipping portfolio and ship covered bonds

The U.S. subprime mortgage crisis (home mortgage crisis) is thought to be major reason of great economic slowdown since 2007. There is a global consensus about causes of the crisis, and both housing bubble and its financial backing, credit bubble, have played a significant role. Therefore, ‘credit crunch’ is interchangeably used for referring the same crisis. Since 2008, several studies investigated the direct causes and drivers (motivators) of the subprime mortgage crisis, and the common component of the failure is frequently mentioned as the banking industry (one remarkable article is written by Joseph Stiglitz titled “The anatomy of a murder: Who killed America's economy?”). Yuliya Demyanyk and Otto van Hemert published a paper titled “Understanding the subprime mortgage crisis” investigated the background of the crisis and indicated some striking conclusions. The financial quality of loans (e.g. credibility of borrower, credit default risk, liquidity risk, etc.) was eroded in six consecutive years before the crisis, and more surprisingly, securitizers (i.e. mortgage securitizers who monetize the mortgage loans) were well aware of the declining power of credibility and refunding capacity. Another confounding conclusion of Demyanyk and van Hemert is that the problems behind the financial failure could be identified well before the crisis while high house prices shaded the monitoring mechanism. The subprime mortgage crisis seems to be a mixture of human error and malfunctioning financial architecture.

While the subprime mortgage crisis sparked a financial chaos by 2008, the shipping business and ship mortgages were not immune to the misguided banking industry. On October 5th 2012, a credit rating institution, Moody’s, posted the following announcement:

“Moody's Investors Service has today placed on review for downgrade the Aa1 ratings assigned to the public-sector Pfandbriefe (public-sector covered bonds) and the Baa1 ratings assigned to the ship Pfandbriefe (ship covered bonds) issued by HSH Nordbank AG (HSH or the issuer), which are governed by the German Pfandbrief Act. On 16 December 2011, both covered bonds were downgraded to Aa1 and Baa1 respectively.

The ratings of HSH's mortgage Pfandbriefe, which are currently on review for downgrade, are not affected by this rating announcement.”

In 2008, the volume of the global shipping loan market (transaction volume) reached over US$ 90 billion, and HSH Nordbank was the leading shipping bank with over US$ 50 billion portfolio (the second is DnB Nor, the leading book runner, with over US$ 30 billion portfolio). Traditionally shipping banks work based on asset-backed mortgage method (ship mortgage). Therefore, the shipping asset value is a critical indicator for monitoring the credit default risk as well as liquidity ratios. The ship covered bonds mentioned on above announcement of Moody’s are a kind of securitization instrument for transferring risks to third parties at some extent. Such kind of bond issues help lenders to raise more funds and take more risks. The critical question here is how to measure the value of ships as a backing of these security bond issues.

There are a number of reasons behind the anomalies on the shipping loan market including risk handling and ship valuation which finally caused the ship mortgage crisis hidden behind the aftershocks of the 2008 crisis. On December 2nd, 2009, an article is published on Business Insider Australia titled “Banks hide shipping losses with -The Hamburg Valuation-” and frankly disclosed motivations behind the valuation game:

“As ship values soared, so did apparent collateral values backing shipping loans. Yet as ship values then collapsed, the collateral disappeared. This threatens to put, and has put, many debtors in breach of banks’ loan covenants.

How can banks avoid coming to terms with the fact that much of their collateral is worth far less than they represent? Scrap mark to market valuation of ships and replace it with a new mark-to-model-driven valuation methodology. Sound familiar?”

The mechanism behind the subprime mortgage crisis and the ship mortgage crisis does not differ much and the fundamental drivers seem mostly same: The imbalance of value and prices, lax regulation on banking industry, deteriorating incentives (e.g. common equity constraint, value at risk approach) and short-sighted governance.

Interpretation of causality through nested instruments and drivers is not a simple one. Rather than benefiting from hindsight, one should dissect the case through each components and legal/substantial evidences to support arguments. Although it is difficult to uncover whole picture and recognize each pieces of irregularities, we look behind the banking industry and shipping firms and investigate the systemic as well as psychological nature of financial meltdown since the global subprime mortgage crisis. The ship mortgage crisis is indicated as a well-hidden banking failure in the shipping business through some system-produced standards such as ship valuation models.

Mortgage loan system and subprime mortgage meltdown

Before analyzing the ship mortgage crisis, it would be useful to review the traditional mortgage system and the subprime mortgage mechanism in the modern banking industry as a state-of-art product of financial engineering. Mortgage loan system basically brings a security instrument, mortgage, for raising large funds. Mortgage ensures trust between lenders and borrowers against insolvency of borrowers. Related legal mechanism is established in almost all free markets, and it allows lenders to possess secured properties such as vessels. The repossession (foreclosure) effort is a coercive power acting as a nudging mechanism in terms of behavioral law and economics (a new perspective in both economics and law making). Once the borrower defaults on the loan or fails to satisfy monitoring instruments (e.g. minimum value covenant), then lender may foreclose the contract and sell the ship to recover the fund raised for purchasing it.

Mortgages in the meaning of collateral or security are first used in 1930s by the regulations of Federal Housing Administration of U.S. The legal framework offered 80% and more of loan-to-value leverage which provided a unique opportunity for Americans to have their own houses (The remaining portion of the value is required from borrower as a contribution to the cost i.e. downpayment). In the amortization period, borrowers pay back the loan with an interest premium till the pay-off date. Finally, the entire ownership of house (or ship) is transferred to borrower while closing the contract.

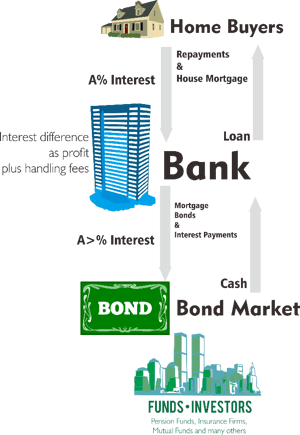

While the traditional mortgage mechanism is widely used in the present banking industry, a financial engineering product, subprime mortgage, has brought a new tier to the system. The term, subprime, refers to borrowers with higher default risk (low credit rating), and prime mortgage is the traditional form of mortgage financing. In the prime mortgage system, banks can convert their risks (credit default risk) to cash through bond issuing mechanism. Mortgage-backed bonds are sold to investors (e.g. pension funds, insurance firms, mutual funds) who gain from repayments of borrowers indirectly (See Figure 1). Lenders still gain profit from these transactions through the difference between interest gained from borrowers and paid for bonds in addition to miscellaneous fees collected at the time of handling the loan agreements.

In the subprime mortgage mechanism, banks create a way of funding risky borrowers. The mortgages collected from subprime borrowers are repacked in collateralized debt obligations and sold in slices based on the level of risk (safe, risky, etc.) The problem behind the mechanism is the uncertain valuations of properties (i.e. houses). When a slowdown slightly hits the economy, the risky (subprime) borrowers begin to fail and turn to be insolvent. Banks repossess houses (mortgages) and sell for recovering the outstanding debt. This simple process may well work when a few of borrowers default the credit repayments. However, if the volume of defaults rises enormously, then several houses will be nominated for sale as a security of the loan. Based on the simple principles of supply-demand framework, larger supply of houses will result in lesser house prices, and the recovered fund extremely declines. Finally, banks cannot recover the debt properly.

Source: Author.

Figure 1. The system of mortgage-backed bonds.

Crisis is sparked through the insolvency of borrowers causes a broader panic and loss of confidence, and the subprime mortgage meltdown of 2008 is also ignited when house prices has fallen dramatically by the panic sales. Therefore, the meaning of security and the risk behind the value of collaterals has attract attention of both financial experts and researchers. The crisis of 2008 is usually thought to be a product of insolvency of Lehman Brothers while it is actually result of more of a fundamental reason: How to value assets when asset prices oscillate in a massive upy-downy market. The valuation problem of houses is not a particular case for banking industry, and the ship valuation is the second tier of entire valuation debate.

Liquidity trap and The Ship Mortgage Crisis

The shipping market boom of 2007 (after previous historical boom of 2004) was the most fruitful and profit making term in the history of maritime industry. Optimism, euphoria and finally irrational exuberance are thought to be driven by repetitive and continuous rise of freight rates (appeal to trend), and these emotional traps triggered less critical assessments and competition neglect on posterior decisions such as ordering new ships or purchasing a second hand asset with historically highest asset prices (Duru, 2013, 2014; Greenwood and Hanson, 2013). In a previous study, I have investigated the impact of boom market climate from the perspective of behavioral economics and have emphasized the lack of practical implications of shipping market knowledge (information-knowledge vs. action-knowledge). One reason of delayed response or lack of awareness on upcoming over supply is associated with the rigidity of supply (response of shipyards, production lag as well as planning failure-delays). The concept of delayed supply response is not a new topic in the economics. Cobweb theory illustrates how delayed supply can cause price fluctuations which is conventionally called business cycles. The underlying principle behind the cobweb theorem is expectations of economic actors are usually backward-looking, and that causes mistaken expectations ignoring the future state of markets or adjusting slowly (i.e. competition neglect in Greenwood and Hanson (2013)).

At the time of market boom (2004~2007), a massive orderbook has been built up by the strong demand for shipping services, ‘non-storable’ shipping spaces. However, there has been another reason which encouraged financing of ships, ‘cheap money’. Lenders were able to have cheaper funds. By the second half of 2007, US Federal Reserve made a critical decision and decreased interest rates enormously (in contrast to the rest of the world including EU, UK and Japan). At the time of market crash, this kind of sudden changes may happen. The uniqueness of 2007 comes from the fact that markets were still enjoying the prosperity and no other country tend to decrease interest rates. Even Euro area increased interest rates slightly. The impact of this unusual interest rate decline is the liquidity trap. Since treasury bills and other secure investment options no longer earn much, large scale investment banks have turned to industries and/or funding other regional/national banks. Cheaper and lax funding trend also sparked shipping finance. Philippe Louis-Dreyfus tells its impact as follows (from Dynasties of the Sea of Lori Ann Larocco):

“Banks put pressure on the shipowners to accept money almost for free, and sometimes offering 100 percent financing with no equity at all. So, banks have played the very awkward, if not the perverse, role in proposing cheap money to shipowners who not only didn’t deserve it, but didn’t really even want it.”

The traditional method of ship financing relies on the collateral security, usually ship mortgage. Similar to house mortgages, shipping banks have an opportunity to repossess the financed ship in case of borrower’s default. Banks can sell and recover the debt. Since ship prices are quite fluctuant, periodical test of asset value is needed to check whether the underlying asset has capacity of recovering the debt in case of a default. The mechanism of periodical asset valuation is ruled by minimum value covenant in loan agreements. If the value of ship declines below the minimum value constraint (e.g. 120% of the remaining debt), then shipping bank forecloses the contract and goes for selling and recovering the debt. Without a minimum value test, it may be too late to foreclose since the asset price may be far below the remaining debt.

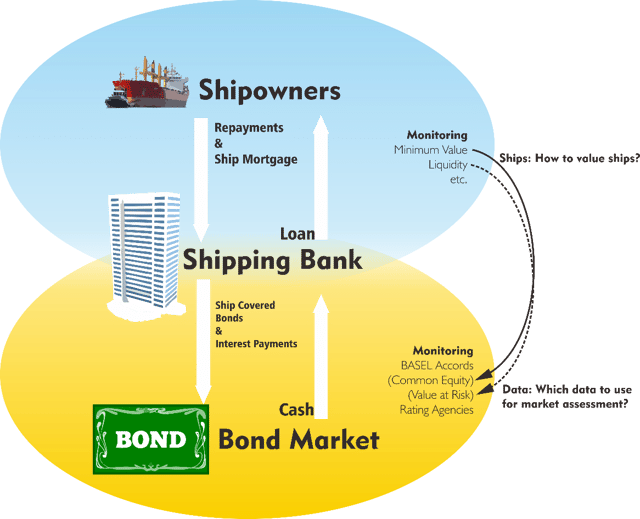

Figure 2 illustrates the entire mechanism of ship mortgages and ship covered bonds. Shipping banks monitor loan agreements (risk assessment) through minimum value constraint, liquidity ratios, among others. On the other hand, financial regulators monitor banking industry through a number of legislative instruments such as Basel accords (e.g. Basel III). Basel accords require some control procedures and risk exposure limits. For example, banks should have a minimum common equity of 7% (Basel III) and review some risk measures such as Value at Risk (VaR) indicator. In addition to the regulators’ stance, independent rating agencies (e.g. Moody’s) review and rate credibility of lenders as well as borrowers.

Figure 2. Ship mortgage system and ship covered (mortgage-backed) bonds.

A critical connection with the shipping loans and common equity arises from Negative Equity debate. When the value of asset (ship) is less than the remaining loan, then the difference causes negative equity. Therefore, the ship valuation method also contributes measuring the equity as an indicator for Basel standards.

About monitoring shipping loans, VaR approach brings some tough questions. Pablo Triana in his mind-blowing book, “The Number That Killed Us: A Story of Modern Banking, Flawed Mathematics, and a Big Financial Crisis”, has criticized the principles behind the VaR method and even blames it as a leading driver of the financial crisis. Although it seems quite numerical and fair, there are several subjective gaps behind its complicated functions. Selection of distributions or dataset is subject to arbitrarily preference of experts. The subjective inputs of risk monitoring are among current debates in the banking industry. Particularly regulators find it difficult to slow down funding of toxic loans at the time of a boom market. The following downturn makes easier while it is usually late for a proper countermeasure.

In the sudden downturn of 2008, ship prices declined largely and the minimum value mechanism raised a serious problem. Shipping banks have had a huge shipping portfolio and most of these assets were under the default risk in terms of contracts while shipowners were somewhat able to pay back. The ship mortgage crisis has been somewhat postponed through the uncertain and tricky nature of ship valuations. There are several reasons of ship valuations (insurance, company valuation, court sales etc.) and several methods of valuation. Mark-to-market valuation is simply the potential price of the ship in the current market state with assumption of potential buyers and sellers. In case of peak market, there would be many representative sales in similar technical particulars, then one may find a very accurate value of the ship. In case of slowdown, it is not easy to find representative sales, then experts tend to estimate prices based on a pseudo-sale scenario. Mark-to-market method is frequently used for minimum value constraint while it has brought a massive default problem. As an alternative, mark-to-model (valuation based on a model estimation) and Discounted cash flow (DCF) methods (also income method) have begun to be used by shipping banks.

As a DCF-based valuation method, the Hamburg Ship Valuation Standard (HSVS) in other words long term asset value (LTAV) is developed and enacted on 6th May 2008 in German Law. HSVS method has been an outlet for German Banks to eliminate massive foreclosures based on monitoring the asset value. In the subprime mortgage crisis, the volume of defaults by subprime (risky) borrowers transferred houses to banks’ ownership while these assets were not able to repay the outstanding debt with the declining house prices. Therefore, mortgage-backed bonds have lost their credibility as well as credit default swap buyers (a kind of insurance for credit default) have begun to write down the insured value. In the ship mortgage crisis, ship covered bonds (ship mortgaged-backed bonds) played a multiplier role. HSVS saved,

Shipping portfolio from massive default which may have ignited further and deeper credit crunch in the shipping industry (very low ship prices, undesirable foreclosures etc.)

Ship covered bonds from insolvency indirectly.

However, the countermeasures did not secured the credit rating of ship covered bonds. The "Schiffspfandbriefe" (ship covered bonds) of HSH Nordbank was first rated as a top, Aaa, by Moody’s, one of the leading credit rating institution, on 3rd September 2007. Then, Moody’s began to review the bonds for possible downgrade and finally the first downgrade to Aaa3 was declared on 6th May 2009. In the following years, Moody’s reviewed Pfandbriefe of several German Landesbanken and their subsidiaries and downgraded the credit ratings many times. European Central Bank (ECB) listed some German banks including HSH Nordbank, Commerzbank AG and Norddeutsche Landesbank Girozentrale for comprehensive assessment in 2013, and HSH posted a loss of 814 million euros in the same year, the biggest since 2008.

Moody’s published a report titled “German Shipping Lenders: Rising Problem Loans May Prompt Net Losses at Some Banks” in December 2013 and indicated “significant asset quality challenges” in 2014. The report also questions the shipping focused banks and indicates “Less diversified banks with significant shipping sector concentrations are the most exposed to persistent stress in the sector”.

International Monetary Fund (IMF) reviewed the German banking industry (IMF Country Report No. 14/216; 21st July 2014) and indicated that

“While work on the ECB’s Comprehensive Assessment was still ongoing, the authorities were confident German banks were generally well positioned for the exercise. They noted the continuous and significant improvement in banks’ capital ratios over the past several years, but agreed that shipping loans could be a source of further impairments”

that matters most

Get the latest maritime news delivered to your inbox daily.

Several investigations showed that the shipping loans are usually toxic and it is quite difficult to avoid risks under the volatile nature of shipping markets. None of conventional countermeasures and financial engineering solutions can precisely settle the fundamental problems of ship valuation and risk assessment. Therefore, we need an outlet for this emerging problem.

---